About Dicker

Dicker Data is an Australian and New Zealand IT distributor. Best described as a mover of boxes they partner with large tech companies i.e Apple, Dell, Samsung, and Microsoft and help distribute their hardware and software throughout Australia and New Zealand. Since its IPO in 2011, Dicker Data has produced returns of 40.5% P.A not inclusive of dividends, while paying out 100% profits to shareholders. CEO and founder David Dicker is the largest shareholder along with his ex-wife Fiona Brown who own 33% and 32% respectively. In a boring industry that has grown at around 6-7% P.A Dicker Data has been able to compound revenue organically at ~20% for the last decade while operating on gross margin of nearly double its competitors.

While not a rollout, they do have a minor acquisition history which includes:

2014- Acquired Express Data for $65m

2021- Acquired Exceed, the largest distributor in NZ for $68m

2022- Acquired NZ-based security distributer, connect and Security which has been rebranded to Dicker Data DAS for $5

Competition

Dicker chooses to focus on smaller customers, as large resellers like Harvey Norman and JB Hi-F have much more bargaining power and consequently offer distributors much lower margins. By picking off the low-hanging fruit Dicker has been able to operate on gross margins of ~9% and profit margins of just ~2.5%, while Synnex and Ingram Micro Dicker’s 2 largest competitors operate on just 5% gross margins with profit margins of ~1.5%. It is in the SME market in which Dicker has around 50% market share compared to around 35% of the Australian market.

2021 company presentation market share:

2022 (includes acquisition of exceed):

Secret Sauce

Dicker’s secret sauce is derived from its management team. Anyone who has come across David knows he’s an odd type. David has done a fantastic job of aligning his management team to think like owners and entrepreneurs and not just business people. David has flagged that, the success of the business has come from management's ability to create the best system for resellers through engagement and partnering together.

Dicker’s success can only be as good as their resellers, and Dicker has created the best end-to-end solution, from financing to profitability, 24/7 customer support, logistics and more to help resellers best succeed.

Jeff Bezos's 2003 letter to shareholders

“Long-term thinking is both a requirement and an outcome of true ownership. Owners are different from tenants. I know of a couple who rented out their house, and the family who moved in nailed their Christmas tree to the hardwood floors instead of using a tree stand. Expedient, I suppose, and admittedly these were particularly bad tenants, but no owner would be so short-sighted”

To me, this quote best embodies Dicker’s management team, a team with a long-term vision and an owner’s mindset. Dicker’s ability to compound the top line at ~20% and gain market share has come on the back of a highly motivated management team competing against 2 large bureaucratic, slow-moving incumbents with tenants, not owners.

David Dicker has Stepped back now although still retaining the title of CEO, COO Vladimir Mitnovetski handles the day-to-day operations, while David moves between NZ and Dubai working on his race cars.

There is no management team on the ASX more incentivised to grow their company with at least 80% of all executive remuneration tied to a percentage of profits.

David lives off Dividends, while COO, Vlad has 100% of his remuneration tied to a percentage of profits.

As of the 2022 annual report management position, ownership (AUD), and tenure:

David Dicker- $481m (CEO/ founder/ Chairmen)

Fiona Brown-$456m (Founder/ board member)

Vlad- $6.9m (COO) 13+ Years

Mary - $2.6m (CFO) 20+ years

Ian -500k (CIO) 10+ years

I don’t know many management teams with 70% inside ownership, and employment tenures of at least a decade.

Inside ownership guarantees no success, but it’s nice to know management is trying and believes in the success of the business.

Opportunity

The opportunity going forward is for Dicker to continue to extend its relationship with resellers and grow organically and acquisitively gaining market share and entering new verticals (i.e recent acquisition into security distribution). The IT market is forecasted to grow at 6-7%, through tailwinds and organic growth, a top-line growth rate of 8-13% P.A is fair for the next ~5 years. Management has flagged growing software revenue to 40% of total revenue from ~25% and while Dicker's day of growing the top line at 20-30% are behind them they are very much in a dominant position in the Australian market to capitalise on the IT tailwinds and continue to grow market share.

Capital Management

Distribution requires large amounts of working capital hence why Dicker finances it through debt, $241m 2022 annual report. Inflation and interest rates resulted in 2022 profit flat while revenue was up 24%, with 14% organic growth. Operating on 2-3% margins doesn’t leave much wriggle room, especially given the 100% payout ratio of profits. Any unexpected expenses/ opportunities (i.e purchase of land/ warehouse) usually results in a capital raising:

August 2022 Raised $71.8m - $50m Institutional, $21.8m SPP Retail

May 2020 – Raised $65m - $50m Institutional, $15m SPP Retail

August 2015 - Raised $45.5m - $40.25m Institutional, $5.25m SPP retail

March 2015 - Raised $40m Corporate Bond offering h

January 2011 - IPO Raised $1m

David refuses to raise equity for acquisitions but believes the best thing to do is take out debt and pay back the loans through raising equity.

Why I Like Dicker Now

Like a lot of companies, Dicker was a Covid hot stock, objectively expensive trading at $15.5 for 45x earnings, 18 months later the business has continued to grow continuing to grow while the share price has fallen 40% to 20x earnings currently trading at $8.27

Valuation

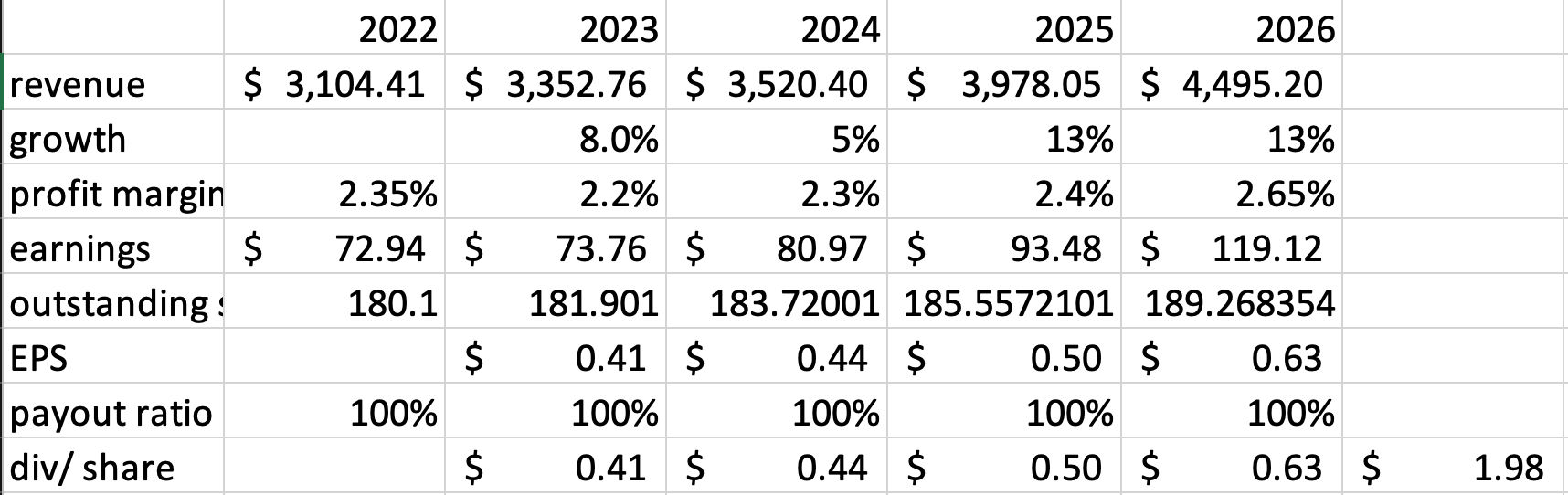

Below is my forecast of what I think Dicker’s Revenue, profit, EPS and dividends will likely be for the next 4 years.

Q1 sales growth was 15%, and I expect the economy to tighten as the year goes and into 2024, rebounding in 2025/26 where they will be able to grow market share and grow revenues at ~13%, above the industry growth rate of ~7% . I accounted for some small dilution of 5% (in line with the previous 5-7 years). Profit margins may have short-term weakness but should revert to the long-term average of 2.65%.

As of the end of the 2022 financial year, Dicker finished with profit margins of 2.35%, down from 2.96% in 2021, 2.84% in 2020, and 3.1% in 2019. Margins have been suppressed by the rising cost of debt and inflation. While I expect these factors to mean revert, I think inflation and interest rates will remain above 2019-2021 levels, resulting in the long-term profit margins of Dicker reverting to ~2.5-2.7%. It is to be noted that high-quality companies always seem to shock on the upside. If you normalise Dickers 2022 earnings with a 2.6% margin they are trading at 18x* earnings. Given the 100% payout ratio with 100% franking credits and the high-quality nature of the business, most investors will buy Dicker for the high-quality stable growing yield. As margins revert I expect the multiple investors will be willing to pay for Dicker’s earnings to be 20+. A PE of 22 would yield investors 6.5% fully franked, with plenty of room for further upside, especially given the growth potential of the business.

Using the revenue, margins, EPS, and dividend forecasts in the figure above, with a PE of 22 results in Dickers 2026 share price target to be $15.89 representing an IRR of 17.7%

What to watch

My valuations will 100% be wrong, but hopefully, it’s directionally right.

Margins: As Dicker expands they may be forced to compete for larger resellers like Harvey Norman and JB Hi-Fi which may result in lower margins as a result of the increased bargaining power they possess. Inflation and interest rates have already affected Dicker’s gross and profit margins I expected them to normalise over the next 2-3 years however it is definitely something to watch closely, the difference between 2 and 3 % margin is 50%!!

Cash Flow: The large amounts of Cap and Op ex needed has resulted in some very lump operating and free cash flow which hasn’t been in line with profit, no red flags for now but definitely something to be aware of.

Management: As previously discussed it’s a people’s business, run by a great management team, the lack of churn and high remuneration gives me great confidence, but if the key success of the business disappears, the people, so will the outlook for the business and my thesis

Recession: A downturn is definitely the biggest short-term risk. Dicker over-earned through the COVID period with the push-forward demand for IT products. Covid’s first lockdown was 3 years ago now and they are still continuing to grow, however, if Australia/NZ does have a recession the question is how far will the top and bottom line fall and the share price. My assumptions are, as seen in my valuation forecast that they will continue to grow due to the nice tailwinds, mission-critical products, B2B model, and reasonable valuation. But there a good chance of short-term weakness.

You might want to wait 12-18 months to see if sales/ profit fall and you can get a 20-30% better price but you might miss the best time to buy in the last ~ 3 years, and the shares be 20-30% higher, Time will tell. After already falling ~45% to 20x earnings, along with a 5% fully frank dividend for a company with a strong long-term outlook it looks very interesting.

First Substack post, subscribing and sharing would be greatly appreciated, hopefully, more ASX small caps to come