Dropsuite offers a suite of solutions for managed serviced providers (MSPs) to back up workplace email and cloud platforms and is capitalising on global digitisation and cybersecurity trends, boasting a market-leading position in M365 backup with substantial room for expansion with just 3% market penetration. Its potential to expand further into new verticals aligns with 26% p.a industry growth forecasts which is all backed by a capital-light business model with vast scalability.

Since its IPO in 2016, it has grown exponentially and isn’t slowing down with revenue, ARR and Profit up 58.3%, 51% and 172% as of the most recent half.

Highlights:

Market leading position in SME M365 backup and recovery

High customer satisfaction, NRR and ARPU growth with <3% churn

Highly scalable business model, only 3% market penetration

High inside ownership

$23m of cash (14% of market cap), no debt

$33.3m of ARR up 44% as of Q3 2024

An MSP is an outsourced IT professional/ team that manages a business IT infrastructure typically for SMEs who don’t have the resources/ need for an internal team.

Business operations

Dropsuite’s value proposition is pretty straightforward, they are a third-party provider of backup and recovery for enterprise email and cloud platforms, ie email, office 365, Google Workspace, QuickBooks, M365 GovCloud. Dropsuite won’t prevent cyberattacks but will ensure that if they occur business businesses data is backed up and can be restored at any time. Backing up M365 via a third party like Dropsuite decreases any risk of losing all business data as it would be inherently risky for business to back up their data on the same platform they host the data. In addition to this, both Google Workspace and Microsoft 365 recommend businesses to back up their data with a 3rd party provider, as a way to cover themselves in the chance of a cyber attack.

Despite this Microsoft recently launched its own backup solution syntex “in competition” with Dropsuite which spooked the market with shares falling 36% in the preceding week following the announcement. Microsoft backup is by far Dropsuite’s largest source of business and Microsoft entering the market has the potential to make Dropsuite’s business redundant. However, Sytntex uses Microsoft’s Azure platform to back up the data while Dropsuite uses AWS. CEO Charif El-Ansari and a number of MSPs echoed the message that using a Microsoft platform to back up another Microsoft platform undermines the purpose of backing up your data for cyber security purposes, with the potential for cyber attacks to compromise the backup as well as it is is hosted on the same Microsoft infrastructure unlike Dropsuite which is hosted on the AWS platform. In addition to this Dropsuite targets SMEs with a price point of $3/ user, compared to Syntex which has a price point of $5-8/ user.

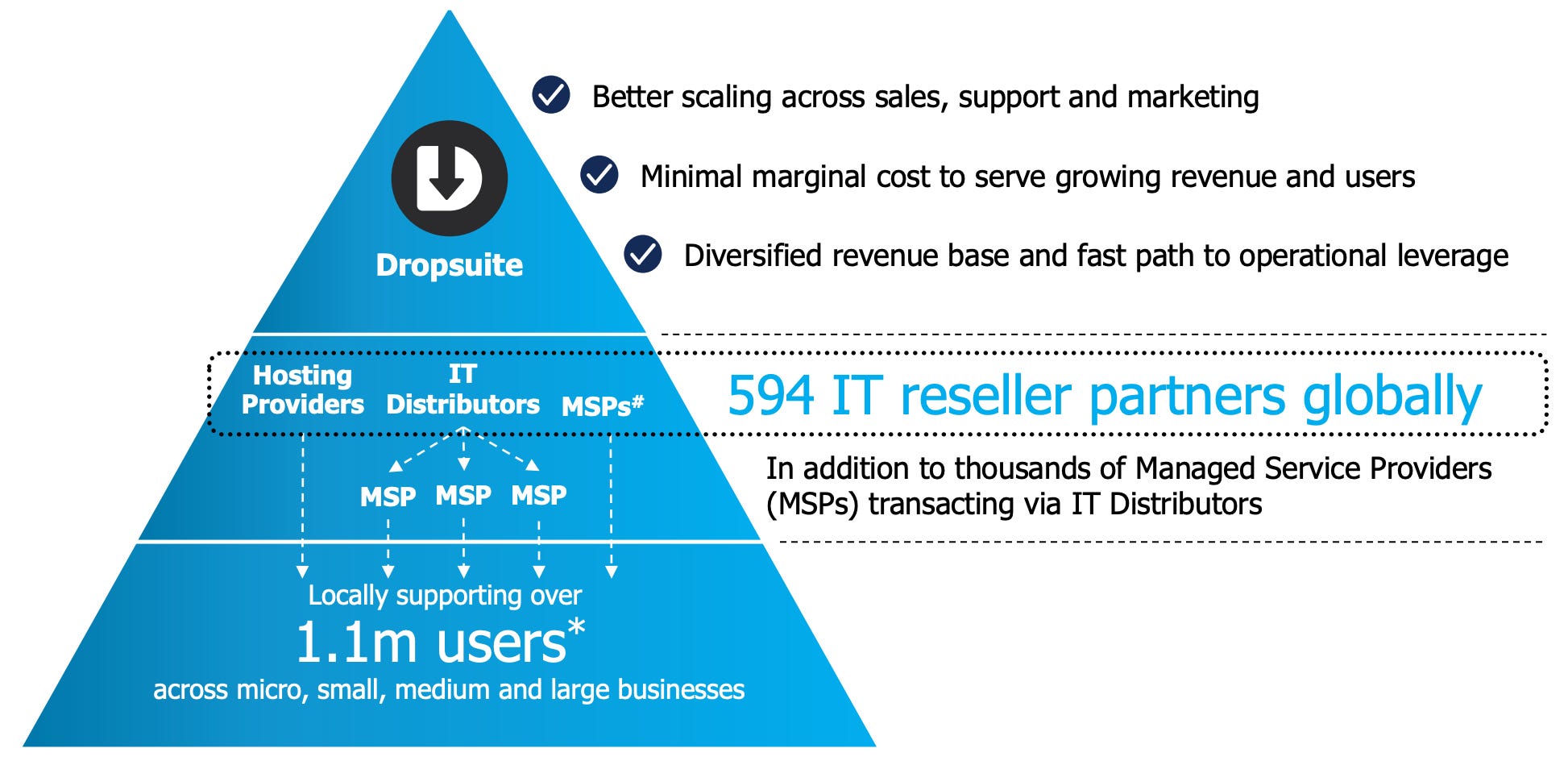

Business model- IT distributors & MSPs

Dropsuite typically sells its product through IT distributors however they do have the ability to sell to MSPs directly and hosting providers. While Dropsuite mainly uses IT distributors around ~60% of Dropsuite customers interact with a Dropsuite sales rep before they buy the product. Dropsuite is installed into the end clients’ systems with support available from the distributor support team who are trained on Dropsuite’s system. Typically Distributors will charge a ~15% fee of Dropsuites sales through their channel, and MSPs will charge end users 20-30% on top of Dropsuites prices. The distributor/ reseller model allows for Dropsuite to scale much more quickly and efficiently, with fewer employee requirements for sales, support staff, and admin ect,.

The large risk with the distributor model is Dropsuite’s reliance on them to adequately promote their product. In 2018 a large partner from Latin America deactivated 420K paying users as they were deemed to not be actively utilising their service, sending Dropsuite's share price down ~60%. Fast forward to today and ~65% of Dropsuite’s revenue comes from its top 10 customers, while they don’t disclose their concentration for each individual customer it can be inferred that there is a significant amount of concentration amongst their largest few partners. I suspect Pax8 is their largest partner and could account for ~20-30% of revenue. The likelihood that a partner like Pax8 cuts off Dropsuite to MSPs like what happened in 2018 is pretty much zero. In Dropsuite’s most recent half revenue growth was 58% with ARR up 51%. Why would a distributor cancel existing and future Dropsuite subscriptions for a product that is a leader in its field, receiving huge amounts of adoption, has the highest customer satisfaction vs competitors and is a source of large amounts of growth for their own business, with a very long way for growth?

I don’t think a distributor would deactivate Dropsuite for the given reasons but Dropsuite's high concentration to some distributors increases the distributer’s bargaining power in negotiating higher margins. As of right now, Dropsuite comes up first on Pax8 when searching for M365 and email backups but if Dropsuite were to not cooperate with a distributor or a competitor offers the distributors better margins the distributors would be more likely to promote their product over Dropsuites.

Competition

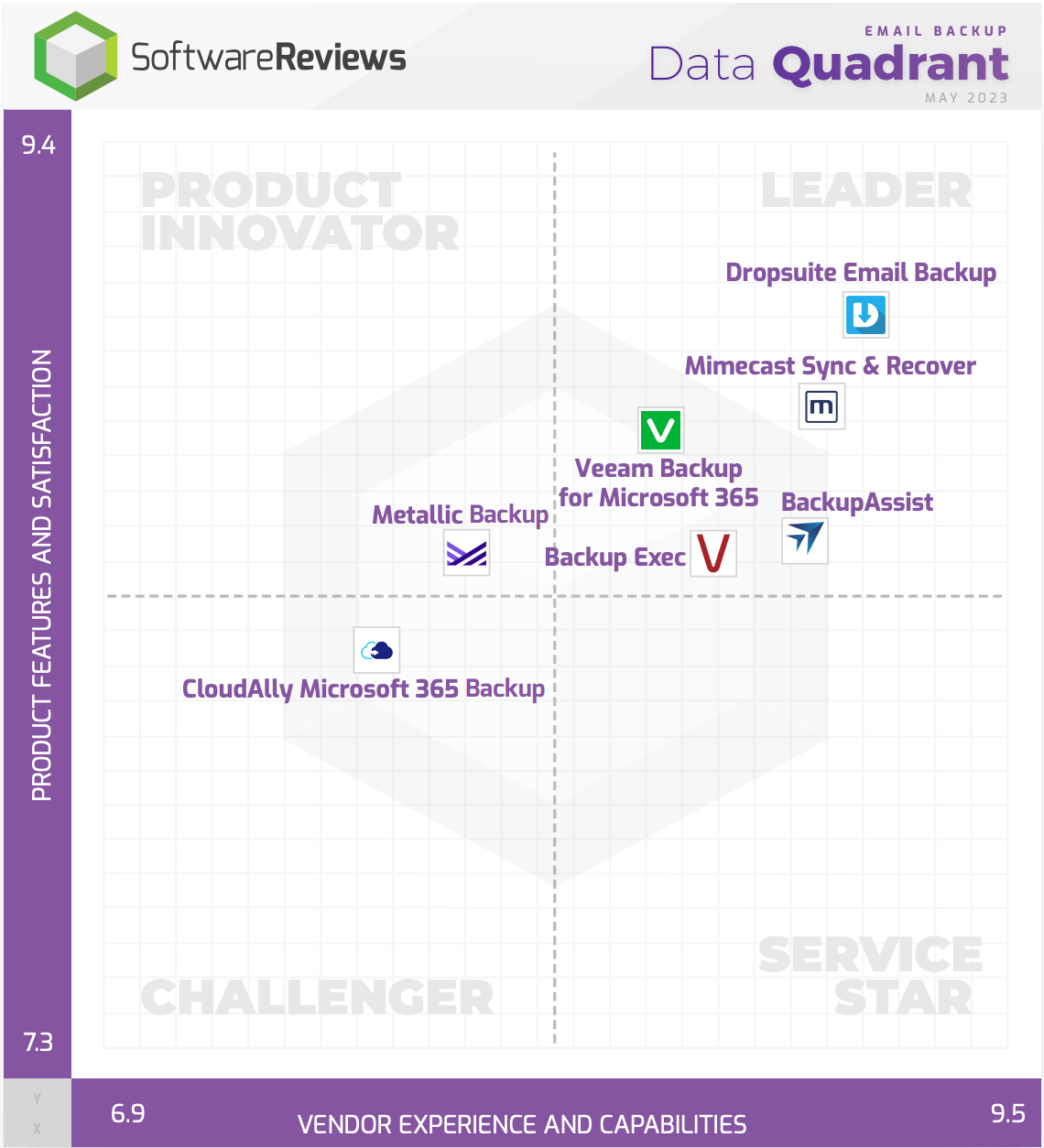

Email and workplace software backup is a highly competitive field with many companies offering slightly different products to different target markets. Dropsuite’s largest competitors are companies such as Datto, Veeam, Afi.ai, Acronis, Druva, MSP365, redstor, unitrends and many more.

You can see in the figure above that Dropsuite is Software reviews top top-rated Backup platform for email, which they have won 3 years in a row.

With ~40 odd direct competitors in their space, it is very hard to get a strong gauge on Dropsuite’s competitive position. Reading through various review websites/documents and MSP forum pages Dropsuite consistently receives top reviews from users, with the highest percentage of positive mentions. From my understanding companies like Datto, and Veem offer inferior products but are much larger businesses, with AFI.ai being Dropsuite’s strongest most direct competitor.

Larger players like Datto and Veeam offer suites of products on a ‘platform’ with email and O365 backup a complementary product to their core business. These sort of competitors target much larger firms or have cheaper pricing and are larger businesses with US$1B+ in revenue but consistently receives low reviews from users as a result. Dropsuite’s main source of edge is their focus on delivering email and O365 backup for MSPs/SMEs, which is typically just one of many products in a stack of IT solutions MSPs use to service their customers.

Dropsuite consistently stands out on all the various review websites and from my understanding, Dropsuite edge comes through its ease of use, user-friendly interface, simplistic implementation and archiving/ search functions along with superior product development (they recently launched QuickBooks online and gov cloud backup solutions).

Qualitative assessments of competitive advantages for companies operating in highly competitive fields are extremely difficult, let alone when they are way out of your depths, however, a good guide is always the financials and SaaS metrics. As you will see below Dropsuite has been able to scale ARR, and ARPU at an extremely high clip while doing it profitability with low churn, healthy margins, and little dilution.

Financials

Even after the hiccup in 2018, with the deactivation of 420k users, Dropsuite has been able to grow revenues at 63% p.a from 2019 to 2022 with the strong growth continuing into 2023 with H1 revenues up 58%, ARR up 51% to $30.4m, and profits up 170% YoY. All growth has been organic with no acquisitions and has been underpinned by strong growth in users and ARPU with users growing from 288k in 2019 to 1.1m in 2023 and monthly ARPU increasing from $1.10 in 2018 to $2.57 in 2023.

As of H1 2023, Dropsuite holds $23m of cash, $20m of which was via a raise in August 2021, however, hasn’t been needed as they turned cash flow positive.

You can see that gross margins are pretty weak for a SaaS Company at only ~66%. The implication of this is Dropsuite won’t be able to maintain 25%+ profit margins, with 8-13% the most likely range, with industry peers generally maintaining margins of ~10%.

Outlook

For the last ~12 months Dropsuite has been looking for a complementary acquisition to its current product suite with the potential for further expansion into Google Workspace Backup. A good strategic acquisition in this space is very lucrative for Dropsuite with the ability to substantially increase its stickiness to users, addressable market, and product offering, with vast synergies and cross-selling potential given their already large customer base. Given the $23m in cash balance, you would expect the acquisition wouldn’t be dilutive to shareholders.

In addition to any potential acquisitions, Dropsuite is continuing to invest in developing/ improving its product offering highlighted by the recent launch of backup for GovCloud and Quickbooks online.

Dropsuites tailwinds:

~84% of companies don’t backup their emails

~90% of all cyber security attacks start with email

3% of 130K MSPs globally use Dropsuite’s products

Back-up industry forecasted to grow at 24% p.a to 2025

MSPs expected to grow at 13% p.a to 2030

Government regulation and recommendations for Google and Microsoft

Valuation

You can see with the given assumptions Dropsuite’s outlook through an investment lens. Given that Dropsuites 2023 is pretty much completed, I assumed 2023 revenues would be $31m and used EV given the large cash balance that will most likely be used towards an accretive acquisition. Dropsuite is very much a trendy stock atm with every small-cap investor seemingly to be on board and consequently, it trades at 5x ARR and 90x earnings. Given the hosting costs and cut distributors take, Dropsuite only manages a ~67% gross margins, in the long run this may improve a bit but the chances of 25%+ profit margins are slim to none, and Dropsuite will most likely maintain margins of 8-13% with the potential for upside at further scale.

What to watch

Acquisitions- There are always many risks with acquisitions; valuation, integration of products and people, dilution, overestimating the expected synergies and so on. Given management already expressed diligence in waiting 12+ months for the right business I expect them not to make a rash decision. A well-integrated acquisition has vast upside substantially increasing Dropsuite’s product offering, stickiness to users, along with many synergies given their strong foothold in M365 backup

Customer concentration- While I think the risk of a large distributor delisting Dropsuite is slim to none given there market leading position, strong customer satisfaction and distributers’ sales benefits from having Dropsuite on their platform, however, there is a risk distributors ask for a higher cut knowing Dropsuites reliance and success.

Competition- Email, M365 and Google Workspace backup is a highly competitive field, and there is always a commodity risk/ a race to the bottom. Most companies offer very similar products, with their own subtleties and while I don’t think it will be an industry and business where Dropsuite is able to maintain 25%+ profit margins due to the competition, the continual changing and development of the IT industry and infrastructure will result in backup solutions having to continually develop there products resulting in substantial but not extreme product differentiation that will allow for industry competitors to maintain a competitive edge

Growth- Trading at 5x ARR and 86x TTM earnings there is a lot of growth priced in, and any sort of decline in growth rates will likely result in a significant rerate

Margins- Given the ~66% gross margins, and industry norms 8-13% are a realistic range that Dropsuite can maintain. The difference between 8% and 12% margins is 50%, and I suspect a large bulk of potential returns for investors will have to come from margin optimisation

Reputation- Reputation is everything, and even more so in the cyber security world, any slip-up has the potential to be devastating for the business