ResMed (RMD ASX, NYSE)

ResMed (RMD ASX, NYSE)

Threat of ozempic and Phillips on RMD

Resmed finished 2023 with revenue up 18%, EPS up 15% with strong growth and in all divisions, despite this the share price didn’t get the news and precidingly dropped 30%+. ResMed now trades at below 25x earnings 49% below its 5 year average multiple- the lowest it has been in some 8 years.

It has been speculated that investors have been spooked off by Novo Nordisk’s Ozempic, a simple needle that ‘cures obesity’. However I think many investor’s are overlooking Resmed largest competitor Phillips re-entering the market and Resmed’s declining gross margins which may be driving the share price lower.

Resmed operations

What does ResMed do

ResMed offers a range of medical devices that treat sleep respiratory conditions from your own home, the most common being sleep apnea. Sleep apnea is a sleep disorder characterised by repeated interruptions (pauses in breathing or periods of shallow breathing), with obstructive sleep apnea (OSA) resulting from blocked airways and central sleep apnea (CSA) stemming from the failure of the brain to signal to muscles to breathe.

It is estimated that around 1 in 15 people suffer from sleep apnea worldwide (900m people), with 50% suffering from severe symptoms. The US is the most advanced market with around 20% of patients living with sleep apnea have been diagnosed, in Europe it is estimated that only 5% of cases have been diagnosis. While these numbers won’t change overnight, Resmed is operating in a severely underpenetrated market and has a long runway for growth.

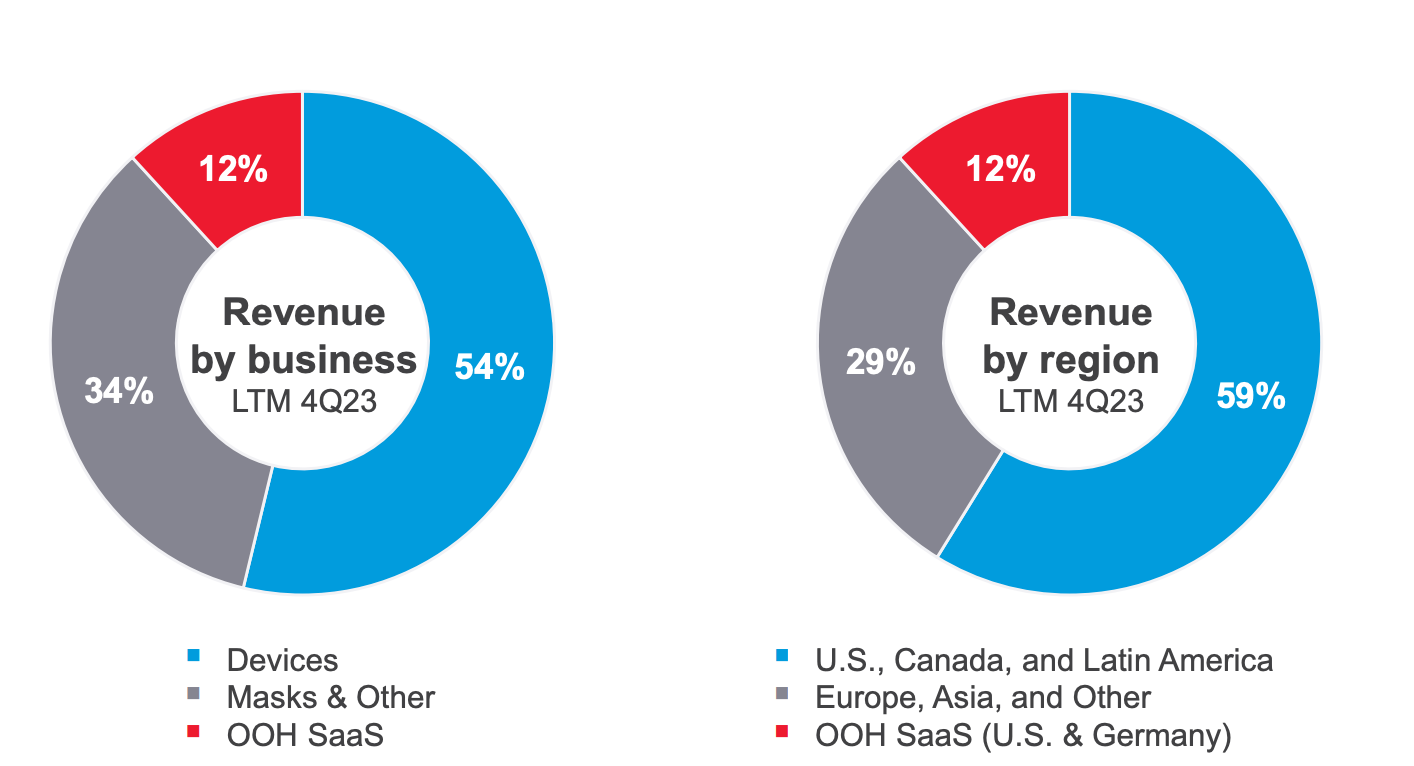

ResMed produce a number of devices to help treat sleep issues, with the CPAP machines and masks being the largest contributer to sales, CPAP machine’s work by delivering a steady stream of pressurised air through a mask to keep the user's airway open during sleep, preventing the collapse of tissues in the throat and ensuring a continuous flow of oxygen. ResMed’s CPAP machines last 3-5 years while masks last around 3 months and are higher margin, all masks are compatible with different CPAP machines. ResMed’s CPAP machine’s are integrated into a software that allows patients and medical professional to monitor and track relevant sleeping information. ResMed also offer’s ancillary solutions to respiratory sleep issues however they make up only a small portion of the business.

The most important relationships for ResMed is the one between the patient the physician. In order to get a CPAP machine you must first undertake a sleeping assessment which has to be prescribed by your doctor, then if diagnosed patient’s will need a prescription to purchase a CPAP machine. Given there is no cure for sleep apnea patients have a high life time value. Customer’s are very sticky due to the network effects, brand trustworthiness and switching costs of the software.

Competitive position

While the tech for these machines is very simple the real competitive advantage for ResMed is in their:

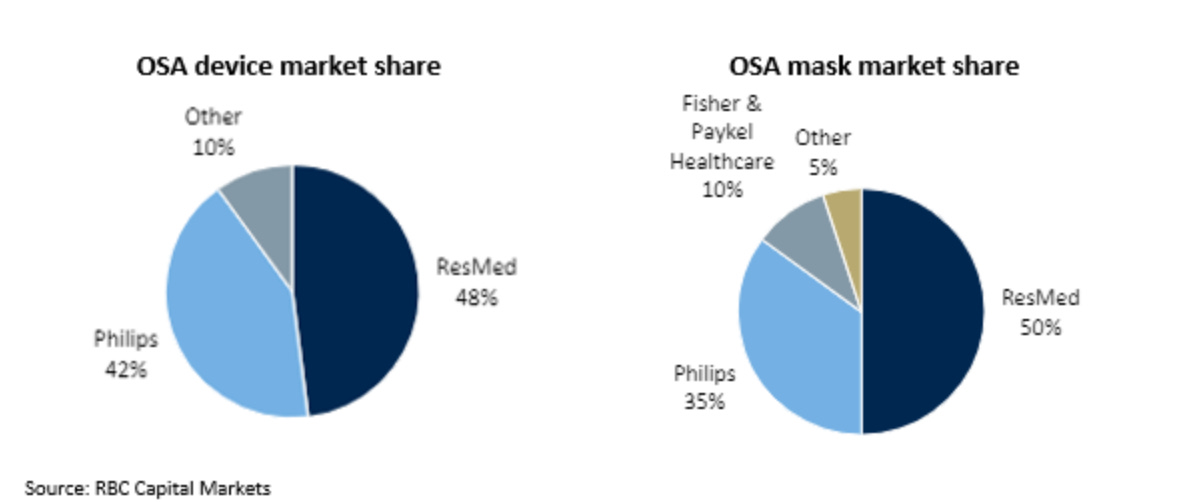

Brand: The medical field is infamous for staying stagnate, customers will typically use whatever is recommended by there physician, and medical equipment is not something people will try and save a few dollars on. ResMed has continued to grow market share, and its estimated they maintain around 55% of the market, and with their major competitor Phillip’s recently recalling some CPAP machine’s ResMed’s brand has never been stronger.

Network effects: The more patients physicians have on the ResMed’s network the more they will recommend ResMed to their patients

Stickiness: There SaaS offering creates key insights for physician’s and patients to track sleeping patterns, and data, as a result customers have high switching costs increasing ResMed’s LCV

Data: ResMed states they don’t sell patients individual data, however they posses the largest network of sleeping monitoring data in the world, which helps ResMed innovate and could potentially be commercialised and licensed off to other healthcare companys.

With relatively simple tech that is easy to copy, ROIC and ROE consistently north of 15% and 20% respectively and margins of 20%+ competitors are more then incentivised to undercut ResMed, however it has not happened in 30+ years, highlighting the strong competitive position of ResMed.

(Figure is from 2021)

Phillips recall

In 2021 ResMed’s largest competitor Phillips which maintained around 40% market share was forced to recall around 3-4 million devices with concerns that sound abatement foam may break down and potentially enter patients air pathways, exposing patients to debris and chemicals while they sleep. Phillips have taken a huge reputational hit and have been unable to make new sales while they replace all there recalled devices allowing for ResMed to gain market share. Since 2020 Phillips’s EBIT has fallen from $1.8B to -$1.8B in 2022. Phillips reentering the market in 2023 is what I think the largest short term risk for ResMed.

After this horrible blunder the market dynamics could revert back to pre 2021 levels resulting in ResMed losing market share and probably a decline in sales. On the other had this may have created a new normal, and customers who were forced to switch to ResMed may stay for good, with more doctors to recommend ResMed’s products. This may be the slow decline of Phillips slowly losing market share every year. After Cochlear’s recall in 2011 I believe they lost market share for around 6 years. While CPAP machines aren’t as serious as hearing implants, the results would likely be a lot worst for Phillip’s given its competitive position against ResMed.

Ozempic

Time to address the elephant in the room, Ozempic, Ozempic works by injecting a solution into your body usually every-week that mimics the natural occurring hormone GLP-1 which simply tells your brain your full. Increasing this hormone makes you feel more full more often, resulting in people eating less and therefore losing weight.

Study’s show people on average people lose 3-5% of their body weight in their first months with obvious decreasing marginal returns are your body fat % decreases. I know of a few girls who has used/ use Ozempic for cosmetic purposes and from all accounts it is very effective, but does have strong side effects.

The US is infamous for having a very poor healthcare system and very high costs for medication. A 2021 study discovered prices of prescription drugs in the U.S. are 2.4 times higher than the average prices of nine other nations (Austria, Australia, Belgium, Canada, Germany, Japan, Sweden, Switzerland and the United Kingdom) and this won’t change anytime soon especially for ozempic given the supply/ demand imbalances. Study’s show that once patients cease taking ozempic they notice a gradual regain of up to two-thirds of the weight they lost, meaning patient’s will most likely will have to be on it for a long period of time. Ozempic doesn’t cure obesity and if people don’t change their lifestyle they won’t see results.

One months supply of Ozempic costs about US$900, with health insurance this drops to around US$25 per month. Patients with type 2 diabetes are eligible for insurance coverage however people wanting coverage for cosmetic or general weight loss have no ability as of now for receiving coverage in the US. The reason for this is Ozempic isn’t FDA approved for general or even chronic weight loss purposes, however physicians can still prescribe it for those purposes.

Around 20% of people who take Ozempic have side effects with nausea, vomiting, stomach pains, diarrhoea the most common symptoms. Studies show that around 16-34% of people don’t lose any weight on ozempic, whole it is the most effective drug on the market, its still no cure.

I think the large craze around Ozempic has been driven by younger females on social media as a solution for cosmetic weight loss. Uptake amongst patients 40+ years old has been a lot lower which tends to be ResMed’s customer demographic. A ResMed CPAP machine costs betweenUS$600-$1000 with a lifespan of 3-5 years, with masks costing US$60-$100 and lasting ~3 months. You would the expect average annual spend for CPAP machine’s and masks to be ~US$600 (not including rebates from governments or insurance), compared to ozempics US$900 cost/ month without insurance which comes with much higher risk.

The fact is 70% of people who suffer from OSA are obese and ozempic has the ability to significantly reduce the number of obese people, drugs like ozempic have been around for a while, while not as effective they haven’t seemed to reduce obesity throughout society. Sleep apnea is far more prominent in older people which I think would be less willing to us ozempic, given the nature of the drug, side effects and pricing point. Everyone I have heard talk about the threat of Ozempic on Resmed’s including analysts, commentators and management have all played down the risk, I wonder weather the risk of Phillips re entering the market or gross margins may have had a larger effect on the sell down.

Financials

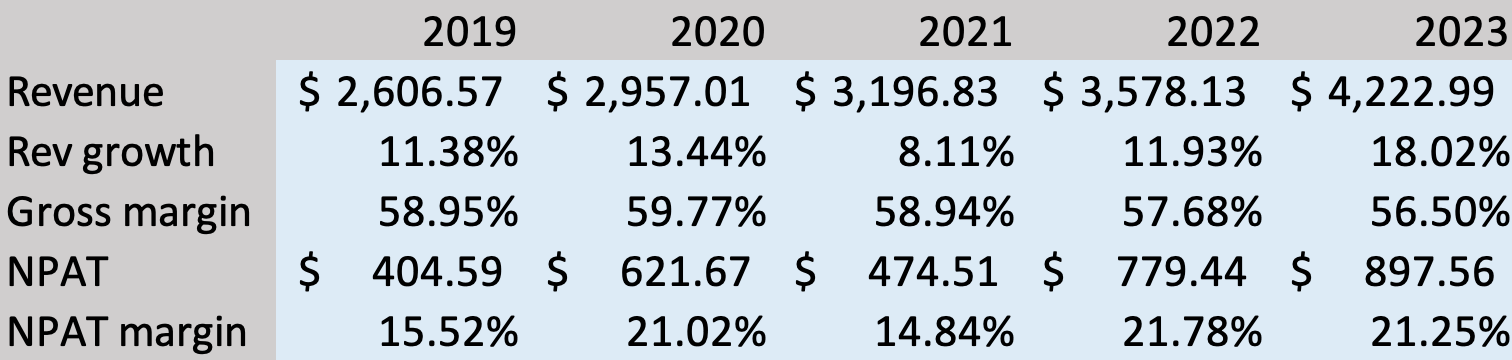

You can see from the figure above that ResMed has had robust growth over the last 5 years, especially capitalising in the last 12 months on Phillip’s recall. 2023 full year gross margin’s took a hit and many analysts were disappointed in the results, which can be explained by a higher mix of CPAP machine compared to masks which are lower margin. Most analysts have been downgrading EPS and price targets but ResMed still sits well below consensus price targets- average price target is $224 / share, significantly below $146 price it currently trades at.

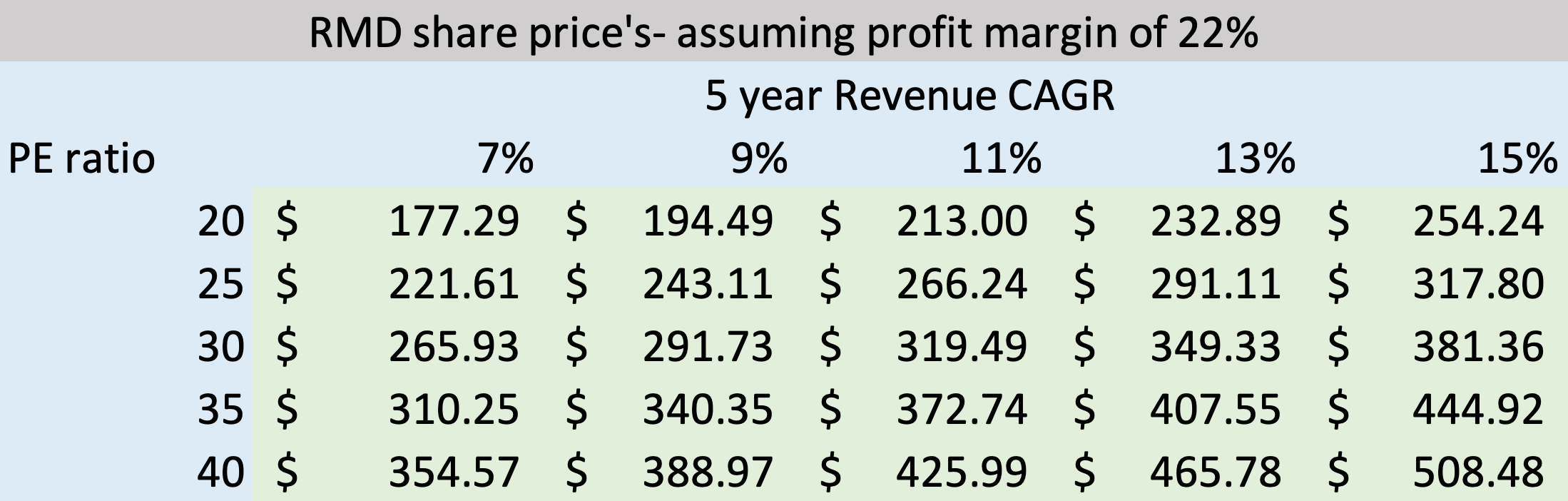

Valuation

RMD currently trades at around 24x earnings. For a company with a long runway for growth, strong tailwinds operating in med tech seems cheap to me in 2023. I think 30x earnings is about fair with the industry average in the US for healthcare products being 43x forward earnings.

You can see above some model scenarios for ResMed in the coming 5 years given the assumption of a profit margin of 22%. With a current share price of US$146 there isn’t too much optimism baked into the price. The figures don’t include any dividends which ResMed has paid out ~35% of profits over the past few years. If you assume that RMD can grow revenue at 11% for the next 5 years, with an exit PE of 30, you would receive about a 17% return p.a not including dividends.

What to watch

Phillips - I think Phillips re-entering the market is by far the biggest short term risk facing ResMed, for the last couple years ResMeds has had no competition and been able to steel market share, but it will be interesting to see in the coming 12+ months, wether Phillip’s can steel back market share, or if ResMed can continue to capitalise off their lost reputation.

Margins- Many analysts weren’t happy with RMD’s gross margins falling to 55% in Q4 and 56% for the full year which is below their long term average of ~60%. It can be explained by a higher mix of CPAP machines which are lower margin than masks.

Ozempic- While I think the threat is very low now, if the FDA changes its approval and more people start taking Ozempic at cheaper prices, there could be a lowering in the TAM of ResMed whihc plays out over decades, but given how underpenterated the market is and the tailwinds of obesity in society I don’t see RMD or obesity going anywhere any time soon.